Rising Deficits: The Problem That No One Wants to Talk About

And that the Republican Tax Bill Will Make Worse

There is a critical long-term problem facing this country that neither political party has shown any interest in addressing: our growing budget deficits and national debt. There were large increases during both the first Trump Administration and the Biden Administration—mostly due to COVID-19 responses, but due to both tax policy and spending bills as well.

Despite this fact, neither party has shown any interest in curtailing the deficit. On the Democratic side, progressives embraced something called “Modern Monetary Theory” that effectively argued that budget deficits are not a problem as long as the economy has the physical resources available to fulfill the spending. As the New York Times explained the theory’s implications, “Deficit spending need not be constrained to recessions, even theoretically. Want to build a road? No problem, so long as you have asphalt and construction workers. Want to feed children free lunches? Also not a problem, so long as you have the food and the cafeteria workers.”

During the first Trump Administration (and in previous Republican Administrations to be fair), the desire for tax cuts trumped (pardon the pun) fiscal accountability. And while Musk and his DOGE bros are getting lots of press and are causing lots of chaos, the actual cuts they are identifying amount only to a rounding error for the deficit calculations.

The fact is that neither party has acted responsibly, and even when they talk about the deficit, they offer simplistic solutions that won’t solve the problem. As the Washington Post said two years ago:

The scale of sobriety that is now necessary means we will need to do a lot more than lawmakers are acknowledging. Republicans falsely claim that the nation’s budget situation would be fine if it just cut back on welfare, waste and foreign aid. Democrats are equally misleading when they suggest it will take raising taxes on big businesses and the rich and perhaps shaving a bit off defense to get where we need to be.

The result of these has been historically high annual budget deficits and a huge increase in our total national debt.

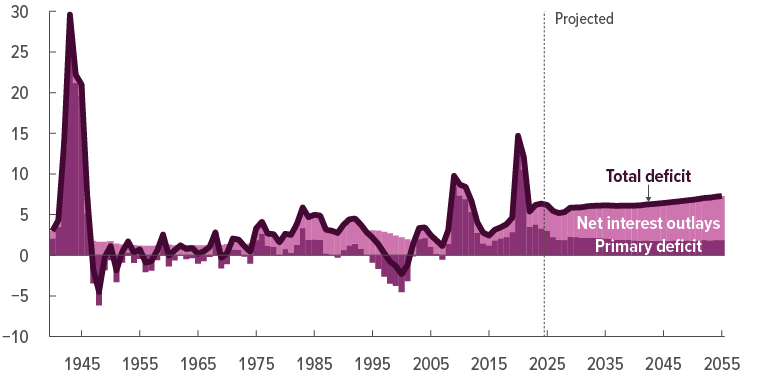

The Congressional Budget Office publishes an annual assessment of the long-term budget outlook. Its most recent assessment is troubling. The chart above is from this assessment. As you can see, there have been spikes in the deficit periodically—most notably during World War II—with more recent spikes during the 2009 financial crisis and the 2020 Pandemic. What is concerning is that years after the Pandemic ended, the budget deficit is at historically high levels that will increase over time. The deficit in 2025 is 6.2 percent of GNP, which is twice as high as the deficit was in 2016, and it is projected to grow to 7.3 percent of GND in 2055. As the Committee for a Responsible Federal Budget notes, this is the highest level of budget deficits outside of a crisis.

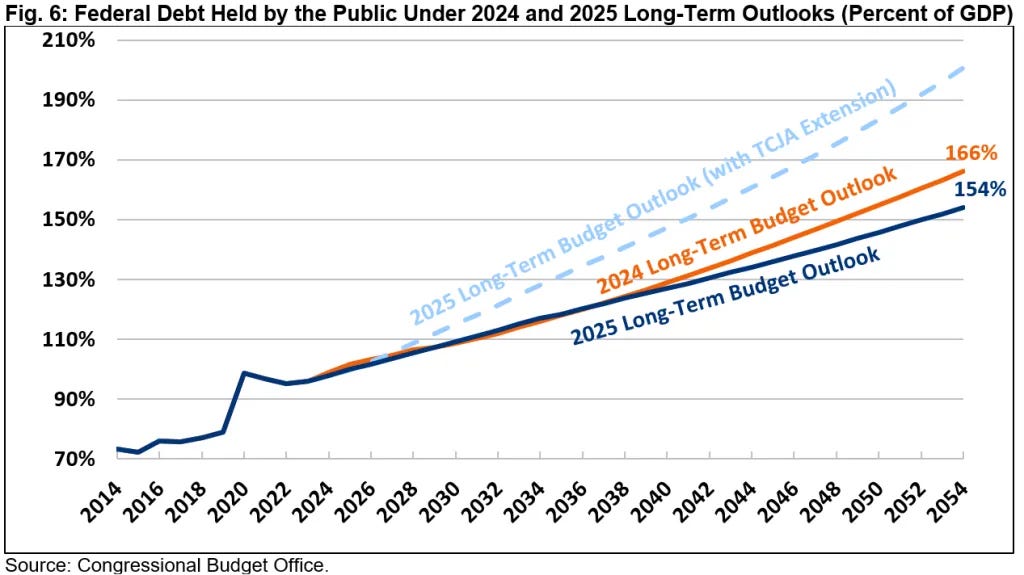

As shown by the graph below, the consequence of these increasing budget deficits is that the national debt held by the public in relation to the Gross Domestic Product exceeds any previous debt in 2029 and grows to even high levels every year after. Think about this—our national debt will larger as a percentage of GDP than was the case in World War II.

But the problem could get worse. The CBO assessment assumes that the Trump First Administration tax cuts go away as scheduled later this year. Trump and the Republicans, of course, plan to extend those tax cuts (and add some new tax cuts). If this occurs the deficit grows even worse.

Critically, this problem is structural. As you can from the chart below, our revenues are consistently below expenditures ,and will be for the near future.

What is causing this structural deficit? The Peterson Foundation has a good explanation. We have an aging population, which is driving increased Social Security and Medicare costs. In addition, U.S. healthcare costs are rising at high rates and, as a result, our healthcare system is the most expensive among the wealthy countries. The CBO projects that federal government spending on healthcare programs such as Medicare and Medicaid will grow from 5.8% of GDP in 2025 to 8.1% in 2055. And one consequence of a rising debt is that interest costs to fund the debt will also rise. Finally, thanks to both tax cuts and tax expenditures (special tax breaks such as tax credits), we simply do not have sufficient revenue.

So why should we care? One major portion of the deficit is driven by Social Security. Right now the deficit in this program—the difference between Social Security taxes and benefits—is being paid out of a trust fund. CBO estimates, however, that in only eight years that trust fund will be depleted, resulting in mandatory across the board benefit cuts unless changes are made. It is important to note that Trump’s proposal to eliminate taxes on tips and Social Security will make this problem even worse by reducing revenue into the trust fund. The Committee for a Responsible Federal Budget explains the impact of the benefit cuts, “Upon insolvency, Social Security retirees will face a 24 percent across-the-board benefit reduction, growing to 28 percent by 2055. We previously estimated that a 21 percent cut for a typical couple retiring in 2033 would equate to a lifetime deduction of $16,500. We could then expect a 24 percent cut to be approximately $18,900.”

Other funds are also headed to insolvency: the Highway Trust Fund in 2028 and the Medicare Hospital Insurance trust fund in 2052.

But the real impact will be even greater. The U.S. will need to fund the debt with more Treasury securities, which will increase interest rates. In addition to further increasing the national debt, this will mean most interest rates (which are pegged to Treasury rates)—such as business loans and mortgages—will increase as well. In addition, at some point, the rising debt will impair the financial markets ability to cover both government and private needs for financing. Wall Street can raise lots of money, but at some point the need to fund the national debt will crowd out private investment. This will dampen economic growth.

To be clear, this is not a call for a “balanced budget". Most economists agree that at lower levels, deficits can actually make sense. This is because many government expenditures—on items like education, infrastructure and R&D—have long term benefits that are appropriate to have future generations (who historically will have higher standards of living than we enjoy now) help fund. And the U.S. has had debt for decades without any harm. The issue now, however, is that the deficits and debt are growing rapidly and are rapidly reaching levels that will cause economic harm.

Sadly, neither political party seems at all interested in addressing this growing problem. And the current political polarization—and the slim majorities in both the House and the Senate would likely make a resolution (which will require both increased revenue and decreased spending) very difficult. Nonetheless, we need to make this issue more prominent in the public debate. Here are some ideas we should be talking about:

The fact that extending the Trump tax cuts will make the deficit even worse needs to be part of the debate. I think this means that none should be extended unless there is alternative revenue. This means that Democrats should stop insisting that only the top bracket cuts not extended. It also means that there needs to a closer examination of our tax system and our budgets. Are the $1.9 trillion in tax expenditures really serving a purpose. Do our tax rates need to be increased? Are there savings to be found in the budget?

The immediate issue—and a large part of the larger problem—is making the Social Security Trust Fund Solvent in the next eight years. The fact that benefits will be cut automatically if the trust fund is not made solvent should motivate action. Both parties claim that they want to protect current Social Security benefits. Given that benefit cuts will occur automatically if no action is taken, they must address the issue to keep their promise. The Washington Post had a really good editorial in 2023 noting that a series of modest revenue and benefit changes would solve the problem. A package of solutions includes increasing the wages and salary subject to the Social Security Tax (now capped at $176,100), tweaking the formula to reduce benefits going to high earners, and gradually increasing the age people can take the full benefit from 67 to 70 at the higher benefit levels (protecting lower paid working class workers who still do physical labor). Right now social security is used as a political point to scare the electorate, resulting in neither party being responsible or productive.

We need to add some disciple to the budget process to require attention to the problem. Harvard Professor (and former Obama official) Jason Furman proposes that all tax legislation must include a reform plan that increases revenues by 0.5 percent of GDP and that there be a Super PAYGO system for all future legislation requiring that savings must exceed costs by 25%.

We need to think outside the budget box for solutions as well. One reason we are facing increasing deficits is the fact with have an aging population with our largest cohort —Baby Boomers—headed to retirement. As a CATO analysis argues, increasing legal immigration will reduce the aging population problem by bringing in younger workers who can support social security and Medicare as well as add more federal revenue. And since health care is a big driver to our deficits, health care reform that seriously address the cost drivers in our health care system. Finally, policies that result in increased economic growth—such as infrastructure and R&D investments—will increase revenue and reduce deficits. We can start by taking serious Ezra Klein and Derek Thompson’s ideas in their new book Abundance seriously.

I get that with all the chaos in the first 100 days of the Trump Administration, the problem of our structural deficit and rising debt is not on anyone’s list of priorities. But the problem is real and we need brave politicians in both parties willing to take it on.